A new state-commissioned report says Michigan drivers are saving an average of $357 per year on auto insurance thanks to the 2019 no-fault reforms. But if you’ve looked at your premium lately, you might be scratching your head. According to the same report, drivers are actually paying about $200 more per vehicle than they were in 2019.

So which is it? And more importantly—what does this mean for your family’s coverage?

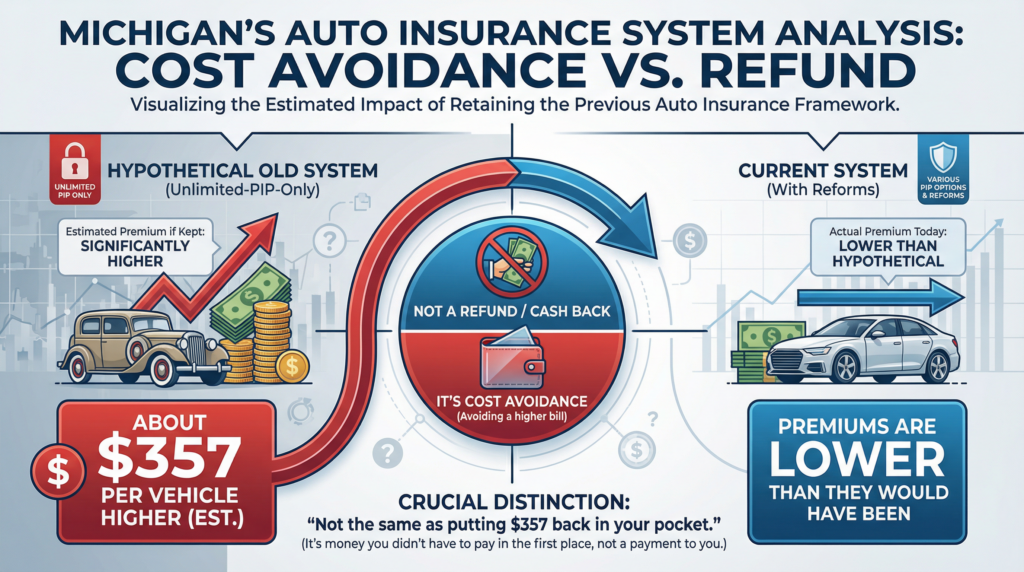

The Real Story Behind the Numbers

Here’s what’s actually happening. The December 2025 report from Milliman, commissioned by Michigan’s Department of Insurance and Financial Services, doesn’t claim your rates went down. It claims they didn’t go up as much as they would have without the reforms.

The analysis estimates that if Michigan had kept its old unlimited-PIP-only system, today’s premiums would be even higher—about $357 per vehicle higher, to be specific. That’s not the same as putting $357 back in your pocket.

Meanwhile, auto insurance costs have climbed nationwide. The Bureau of Labor Statistics reports that national car insurance premiums are 55% higher than pre-pandemic levels. Michigan hasn’t escaped that trend, but the state’s increases have lagged behind the national average—which supporters say proves the reforms are working.

What Actually Changed in 2019

The biggest shift was giving Michigan drivers something they’d never had before: a choice in their Personal Injury Protection (PIP) medical coverage.

Before July 2020, every Michigan driver was required to carry unlimited PIP coverage—which paid for all medical expenses after an accident, for life if necessary. It was comprehensive protection, but it also made Michigan one of the most expensive states in the country to insure a car.

Now, drivers can choose from several PIP levels: unlimited coverage, $500,000, $250,000, $50,000 (for Medicaid recipients), or opt out entirely (for those on Medicare). Lower PIP means lower premiums—but also less protection if you’re seriously injured.

According to the Michigan Catastrophic Claims Association, nearly 70% of drivers still choose unlimited PIP. That means most families either prefer the protection or simply haven’t revisited their policy since the reforms took effect.

Three Questions Every Michigan Driver Should Ask

Whether you made a PIP selection back in 2020 or your policy just auto-renewed with the same coverage, now is a good time to take a fresh look. Here are three questions worth considering:

1. Do you know what PIP level you’re currently carrying? Many drivers chose a coverage level years ago and haven’t thought about it since. Your needs may have changed—especially if your health insurance situation is different than it was in 2020.

2. Does your health insurance cover auto accident injuries? Some health plans exclude or limit coverage for car accident injuries. If yours does, a lower PIP level could leave you with significant out-of-pocket costs after a serious crash. It’s worth checking the fine print.

3. When did you last compare rates across carriers? With premiums rising industry-wide, the gap between what different insurance companies charge for the same coverage has widened. An independent agent can shop multiple carriers to find you the best rate for your situation—something you can’t do with a single-company agent.

The Value of a Policy Review

Michigan’s auto insurance system is more complicated than most states. Between PIP choices, coordinated vs. uncoordinated coverage, bodily injury liability limits, and uninsured motorist protection, there’s a lot to navigate.

That’s where working with a local independent agent makes a real difference. We can review your current coverage, explain your options in plain English, and shop across multiple carriers to find the right balance of protection and price for your family.

And if bundling your auto and home insurance makes sense, that’s often where the biggest savings come from—averaging around 19% off for Michigan families who combine policies.

Take the Next Step

The debate over whether Michigan’s reforms “worked” will probably continue for years. But you don’t have to wait for the verdict to make sure your own coverage is right.

If it’s been a while since you’ve reviewed your auto insurance—or if you’re not sure whether your PIP level still fits your needs—we’re happy to help. At Tucker Insurance Agency, we’ve been helping Canton and Southeast Michigan families navigate these decisions since 1970.

Get a free quote or call us today at 734-697-5544. It costs nothing to compare.