Michigan families are getting hit from both sides right now. Auto insurance climbed 12% in 2025 alone, vaulting the state to 4th most expensive in the country. Home insurance jumped even harder — up 57% between late 2024 and late 2025, according to Bankrate analysis. If you’re feeling it at renewal time, you’re not imagining it. But here’s the number most people don’t know about: the single biggest discount available to most Michigan homeowners may be one they’ve never actually checked.

The Bundling Discount — and Why Most People Get It Wrong

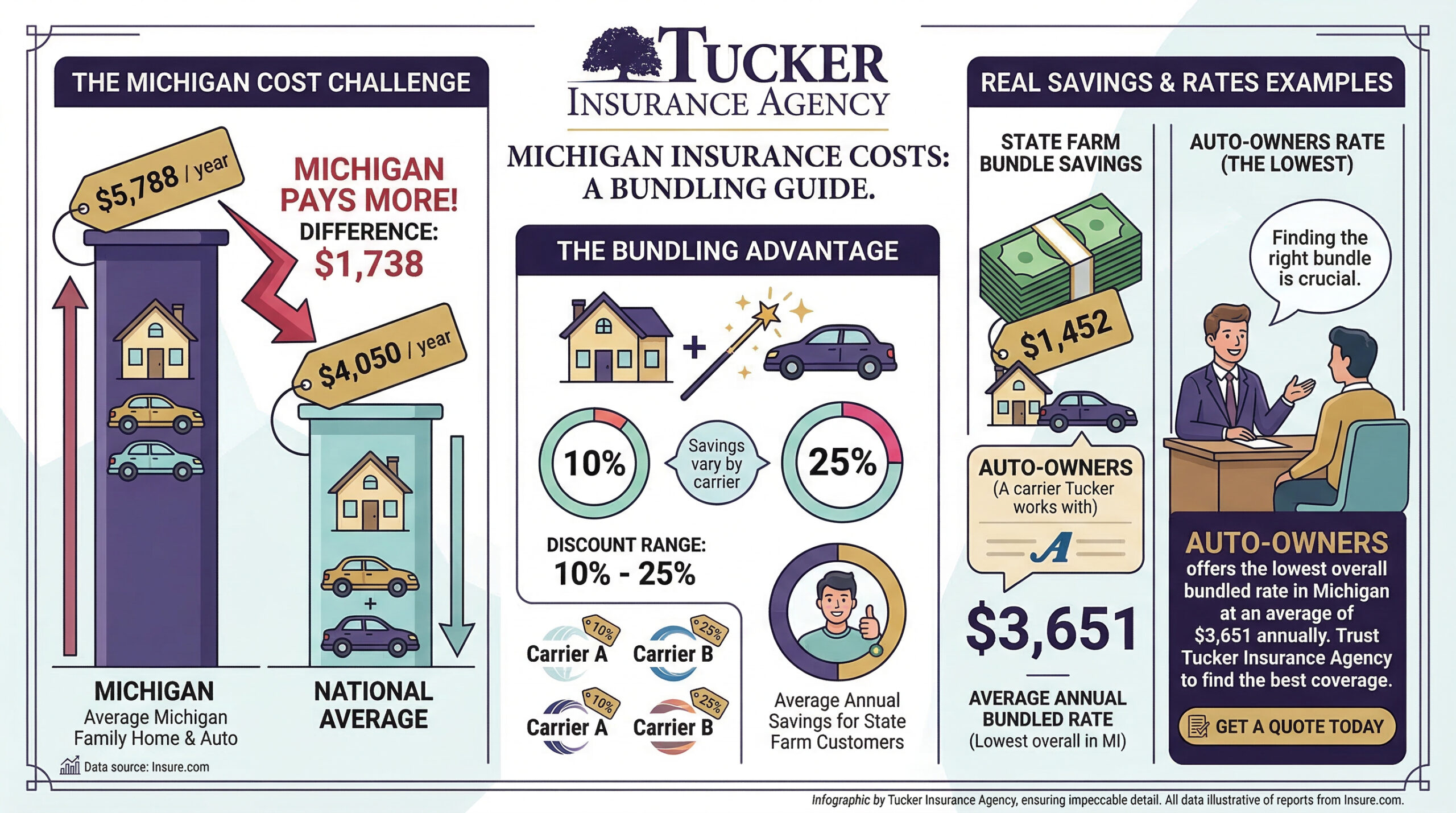

Bundling your home and auto insurance with the same carrier is one of the most widely advertised discounts in the industry. What’s less advertised is how much the outcome varies depending on which carrier you bundle with — and whether your current carrier is actually the right fit for both policies.

According to data from Insure.com, the average Michigan family pays around $5,788 per year when combining home and auto insurance — well above the national average of $4,050. Bundling discounts in the state range from 10% to 25%, depending on the carrier. State Farm’s average bundle saves customers $1,452 per year. Auto-Owners — one of the carriers Tucker Insurance Agency works with — offers the lowest overall bundled rate in Michigan at an average of $3,651 annually.

Those are meaningful differences. And they don’t happen automatically just because you bundle — they depend on landing at the right carrier for your specific home, your specific vehicles, and your specific situation.

The Problem With How Most People Bundle

Most Michigan families bundle the way they ended up insured in the first place: they called one company, got a quote for both policies, and accepted the package. That’s not necessarily wrong — but it means you’ve only seen one carrier’s math.

Here’s what makes this more complicated in Michigan specifically: the cheapest carrier for your home may not be the cheapest carrier for your auto, and vice versa. A carrier that offers a deep bundle discount may still charge more total than two separate, well-shopped policies with different companies. As insurance data from Jerry notes, bundling with the same carrier isn’t always the cheapest option — pairing the best home rate with the best auto rate from different carriers can result in a lower total cost.

That’s a nuanced calculation. And it’s exactly the kind of analysis most homeowners don’t have time to run on their own.

What an Independent Agent Actually Does Here

This is where working with a local independent agent changes the math entirely. Rather than showing you one carrier’s bundle and calling it a day, an independent agent can compare multiple carriers simultaneously — looking at your home policy and your auto policy across different companies at once.

That means Tucker’s team can answer a question your current insurance company literally cannot: “Is there a better combination out there for our family?” A captive agent — one who only sells for a single company — can’t offer that comparison. We can.

This matters even for families who are already bundled. Rates have shifted significantly in the past 12–18 months. A bundle that made sense in 2022 or 2023 may no longer be the most competitive option for 2026. If your renewal notice has arrived with a number that surprised you, that’s a signal worth acting on before you auto-renew.

A Few Signs It’s Time to Review Your Bundle

You don’t need a crisis to justify a coverage review. Any of these situations is a reasonable trigger to call us:

Your home and auto policies are currently with different companies. That’s the clearest sign that a bundle conversation hasn’t happened yet — and there’s potential savings sitting there waiting. Your renewal came in higher than last year. Both home and auto are trending up in Michigan; if your insurer raised both, you may have room to shop. You haven’t compared rates in more than 12 months. The market has moved enough in the past year that what was competitive in early 2025 may not be today. You’ve had a life change — a new vehicle, a home purchase or renovation, a teenager about to start driving — that changed your coverage profile.

What to Expect When You Call

The conversation is straightforward. We’ll ask about your current home and auto policies, your coverage levels, and any recent changes to your property or vehicles. From there, we run comparisons across our carrier partners — including Auto-Owners, Progressive, and others — and show you what combinations look like side by side. There’s no obligation and no pressure. We’re here to help you make a confident decision, not a rushed one.

As we’ve been telling Canton and Southeast Michigan families since 1970: it costs nothing to compare. That’s still true.

Take the Next Step

If you’re not certain your current bundle is the best available combination for your home and auto — or if your home and auto are still with different companies — a quick call could change that. Tucker Insurance Agency works across multiple top-rated carriers to find the right fit for Southeast Michigan families.

Get a free quote today or call us at 734-697-5544. We’re here Monday through Friday, 9 AM to 5 PM.